Exporting the American Dream

Tokenization is American exceptionalism.

The United States, through blockchain, will be the world’s greatest financial exporter, and American capital markets will become its most powerful export.

In May of 2026, the SEC announced the plan to introduce an ‘innovation exception’ for tokenized securities, effectively allowing synthetic stock derivatives under what is expected to be a very light regulatory structure.

This is a great step in the right direction: and I hope, and in some sense expect, the administration to continue championing tokenization. Tokenization, such as stablecoins and onchain equities, is hands-down one of the best tools for American dominance globally.

I’m not sure to what extent this administration has realized the above yet, but assuming they do realize it and maintain relaxed, pro-innovation regulation accordingly, we’ll see incredible growth.

Tokenization is effectively enabling the export of American capital markets to the rest of the world, and we’re already seeing countries in which their local economies are suffering, or stagnant, benefit from this.

A fun name I’d like to give this property, the expansion of American economic influence through tokenization, is “Financial Manifest Destiny.”

If the world wasn’t already dollar-dependent enough, it will be, but even in a further sense than just relying on the U.S. dollar for trade: through the average person participating in U.S. markets via tokenized equities.

I’m not even sure local currencies within tier-two and tier-three countries will remain dominant in their respective regions within a decade. The U.S. dollar, and the U.S. stock market, is often the better consumer choice in many markets with inflation and poor capital control, and stablecoin adoption is already reflecting this.

And fortunately blockchain doesn’t care whether or not it pleases a local government that their population is slowly moving their assets to USD or investing in U.S. equities onchain. This is fundamentally the most impactful usecase of blockchain (rather than speculation on ponzi schemes, shockingly).

Crypto has always been valuable partially because of its ability to be a regulatory arbitrage, this will continue to be the case in regards to global individuals getting their hands on USD and American equities.

Tokenization will succeed primarily because of its magnitude as a tool in expanding American social and economic influence: the U.S. government has enormous incentives to support this technology.

Equities being tokenized are the natural next step beyond stablecoins. Rather than simply exporting the dollar, you bring large swaths of foreign populations into the U.S. stock market, because it offers potential returns that these local economies simply cannot deliver.

Two core problems are solved with tokenization:

- Protecting purchasing power, through USD stablecoins (hedge on local currency inflation).

- Participating in growth, through tokenized equities (as the U.S. economy experiences some of the most consistent long-term growth among the developed world).

I doubt Satoshi Nakamoto originally intended for his invention to be used as a means of economic expansion for the United States, nor would he likely be very happy with that being the case, but this is how it’ll end-up. Unless, of course, Satoshi Nakamoto is actually the CIA as some speculate, in which case I’m sure they’re ecstatic.

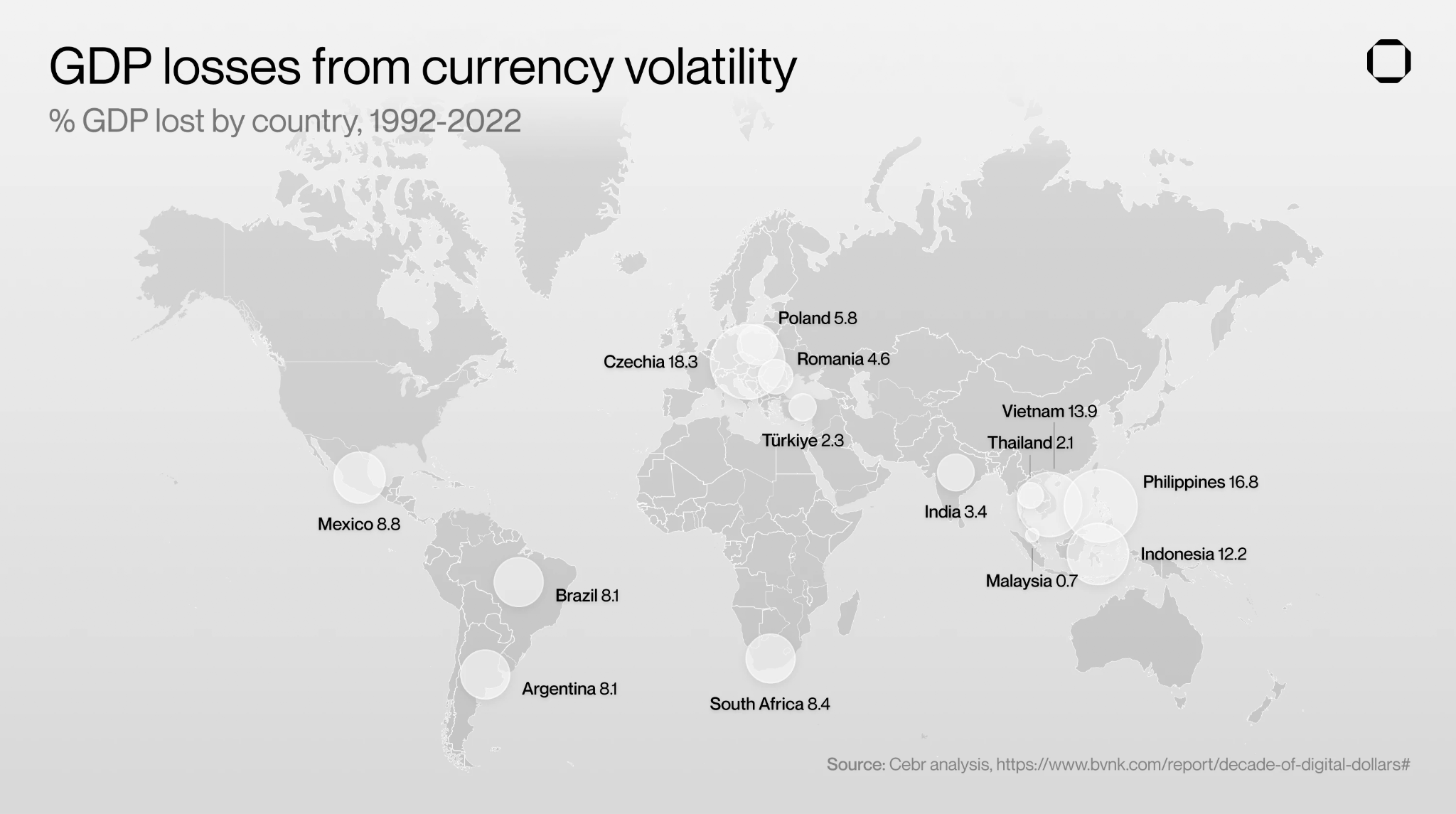

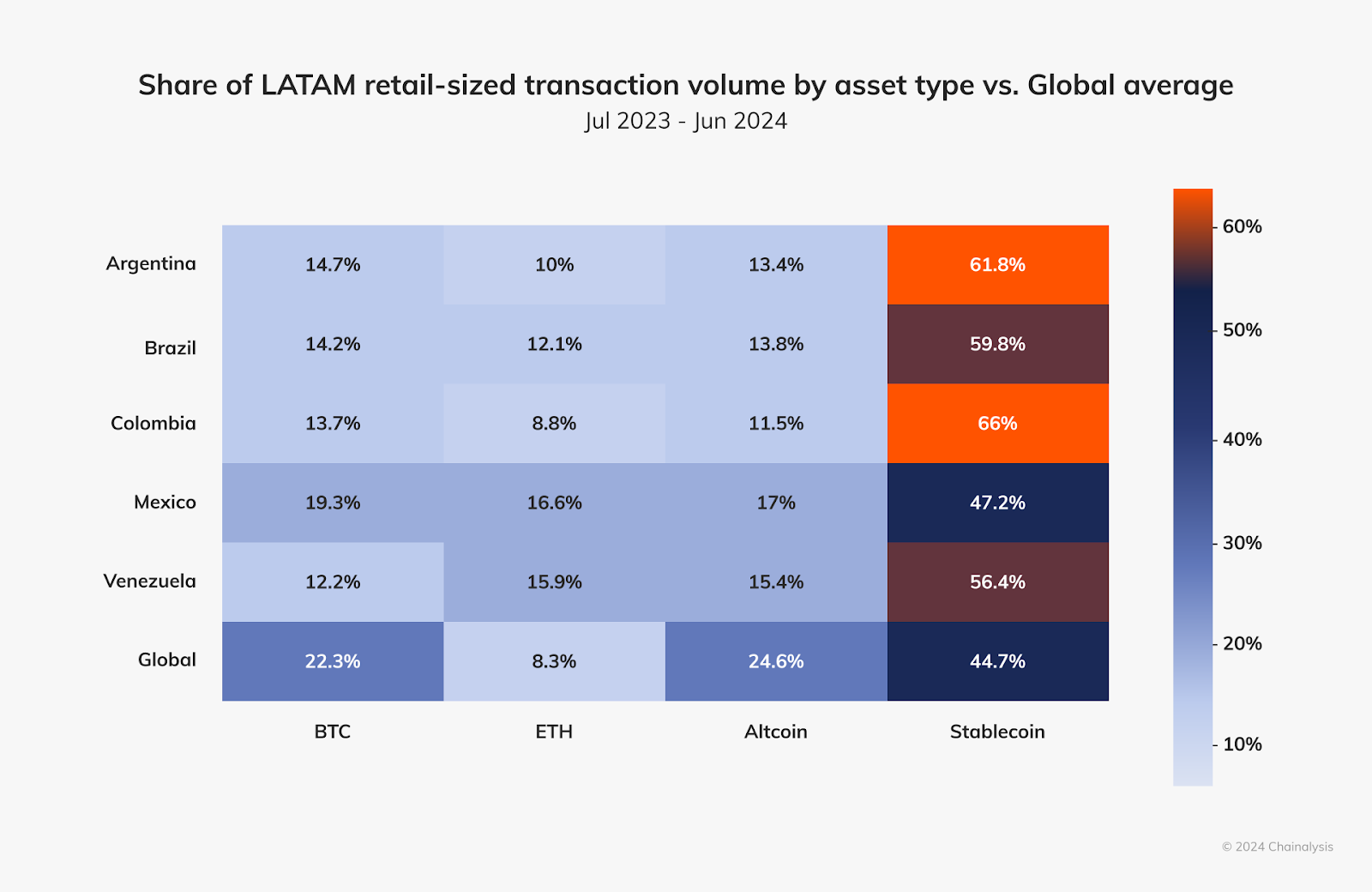

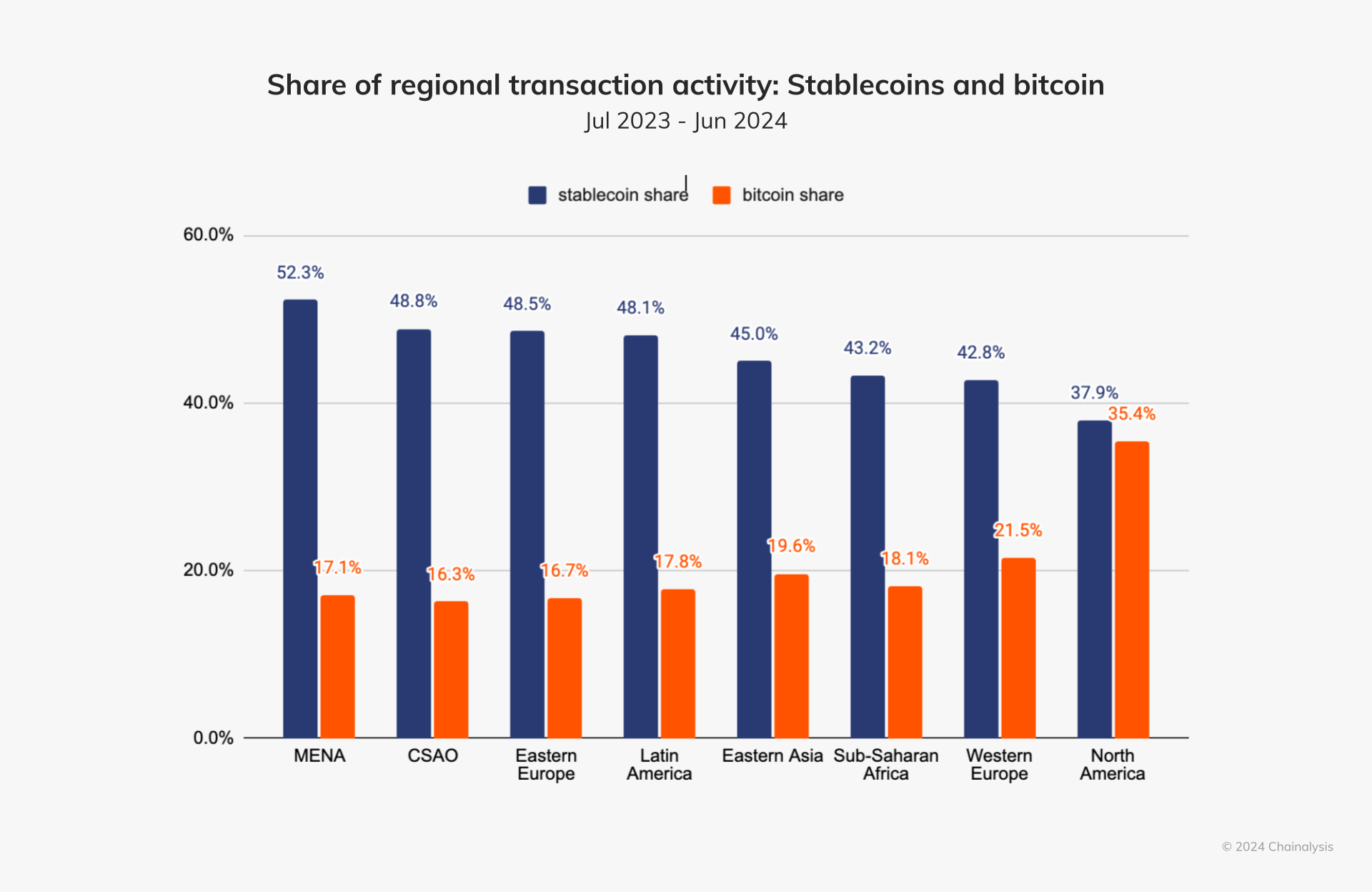

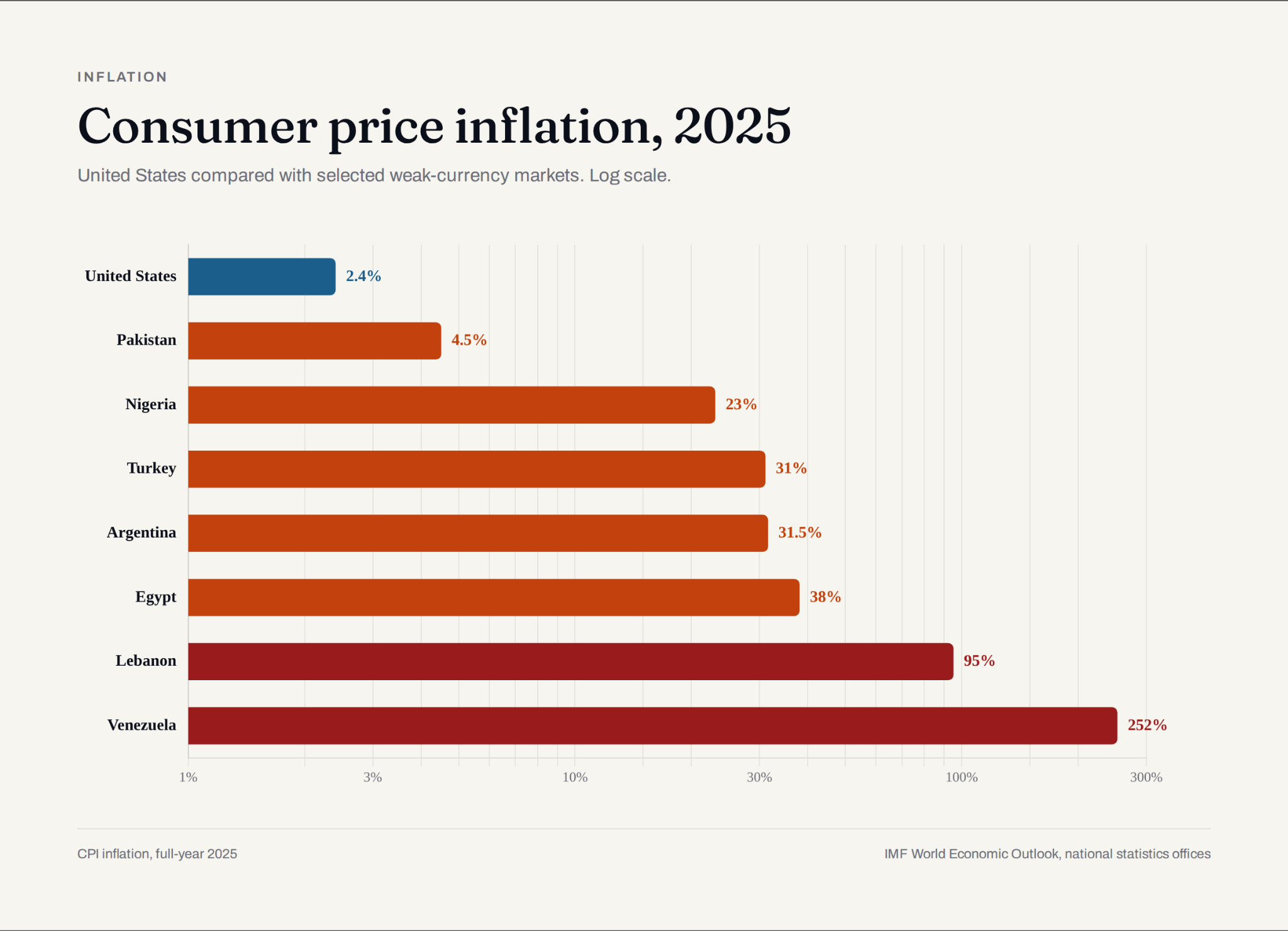

Many will argue that it’s not a good thing primarily from the perspective of limiting American influence, but even if you dislike the United States, you can’t deny the likely quality-of-life improvements, as demonstrated with some of the data below.

(thanks for the fancy graphics, Opus 4.8)

To extend the stability and growth of the U.S. economy that those of us living here enjoy to the rest of the world is only beneficial for those taking advantage of it.

It’s no secret that the world’s elite deal and save primarily in USD, and participate in U.S. markets. Why shouldn’t the average person have the same ability?

The downstream effects of moving a large chunk of the world’s population to the U.S. dollar and (although to a lesser degree) U.S. equities are significant in a way that’s hard to articulate, but I’ll try.

Financial Manifest Destiny

When talking about tokenization in the context of improving American dominance, we can break it down into two categories:

- Currency dominance: improved by stablecoins, but simultaneously already the strongest among these categories.

- Capital-market dominance: through tokenized equities, move global consumer savings to the U.S. stock market.

The U.S. dollar is already dominant for international trade, but stablecoins fill a gap when it comes to consumer savings and spending.

It’s true that, in many countries, people hold physical U.S. dollars as a means of saving while their local currency is subject to endless hyper-inflation: this shows that there’s clearly a “demand for USD as a store-of-value,” and this is where stablecoins are already seeing the most usage, from my understanding.

Although a growing trend will come in the form of USD as a means of exchange in foreign economies. I expect that, assuming further stablecoin penetration, most local businesses will begin to accept stablecoins (bullish on stablecoin POS companies!), and if a large portion of a local population is saving in USD, this will naturally extend to spending.

And thus foreign economies slowly shift to being partially, if not mostly, dollar-denominated over time.

As a result global dependence and demand for the U.S. dollar increases proportionally.

Regarding capital-market dominance, this is where it gets more interesting for me. Dollar-dominance is already established in many forms, although not as deeply engrained as the structure I described above. Inversely, in the context of consumer penetration, U.S. capital-market participation is not as mature.

Many developed countries (Singapore, South Korea) already have local options for trading U.S. equities, although in the same regions that stablecoins will find most success in, tokenized equities will find equal success in.

Tokenized equities are powerful for a similar reason that USD as a store-of-value is powerful, in that it provides a (relatively) secure position for growth. As I mentioned earlier, the rich-and-powerful of the world already trade U.S. equities disproportionately, and so this is extending this proven demand to the average person, who, while they won’t be trading millions in volume, will undoubtedly move capital into U.S. equities at an increasing rate over time.

This is why I consider tokenized equities a great example of Freedom Technology!

Functionally, for the U.S., this is funneling consumer savings globally into U.S. capital formation. In-turn increasing demand for corresponding assets, deepening U.S. market liquidity, adding more incentive to build companies in the states, and so on.

Although, it’s not all good from the standpoint of the U.S. government. As I mentioned, blockchain does a great job of being a regulatory arbitrage. Because it’s hard to regulate and operates mostly independently from local laws, it’s also hard to enforce things like sanctions and foreign capital-control.

But, at the same time, there’s sort of a logical loop here. From the standpoint of the U.S. government: if I enforce strict regulations on tokenization and try to ‘centralize’ it to retain foreign capital-control, companies will just leave the states and build this anyway (it’s blockchain, after-all).

So, from my perspective, the best option is to take the win and allow the flower of innovation to blossom.

With great power comes great responsibility. And freedom means freedom, so I think this is an acceptable downside for the resulting upside outlined throughout this essay.