T+Open: My Solution to 24/7 Trading

It’s consistently shocked me that no one has delivered a good implementation of 24/7 tokenized stock spot trading yet (spot being the key-word). The flexibility of transferable equity-linked tokens allows for a relatively simple implementation of trading over the weekend.

Weekend trading hasn’t yet been delivered for two reasons:

- No liquidity.

- No reliable, hedgeable means of pricing assets.

For the first problem, the core of it is simply that no one is willing to buy your stock on Saturday and Sunday because of the second reason: there isn’t a great way to price it, and thus any counterparty that buys is taking risk.

As the counterparty buying your stock: if I’m arbitrarily pricing it at $100 on Saturday, but the open is actually $90, I’ve lost $10 on that position, unless it’s hedged, which until recently there wasn’t a great way of doing this either.

The same is true for that counterparty selling the stock, and the consumer buying it.

The second problem, lack of an accurate pricing engine, leads to the first.

So, how do we deliver trading on those precious 48 hours that we’ve been missing for 234 years? Well, if we can find a reliable way to price these assets, and a way to hedge these positions such that they’re price-neutralized, it can work.

We’ve built a system for this on Street that we call “T+Open,” I’ll explain some of the fundamental mechanics here.

Hedgeable Reference Markets

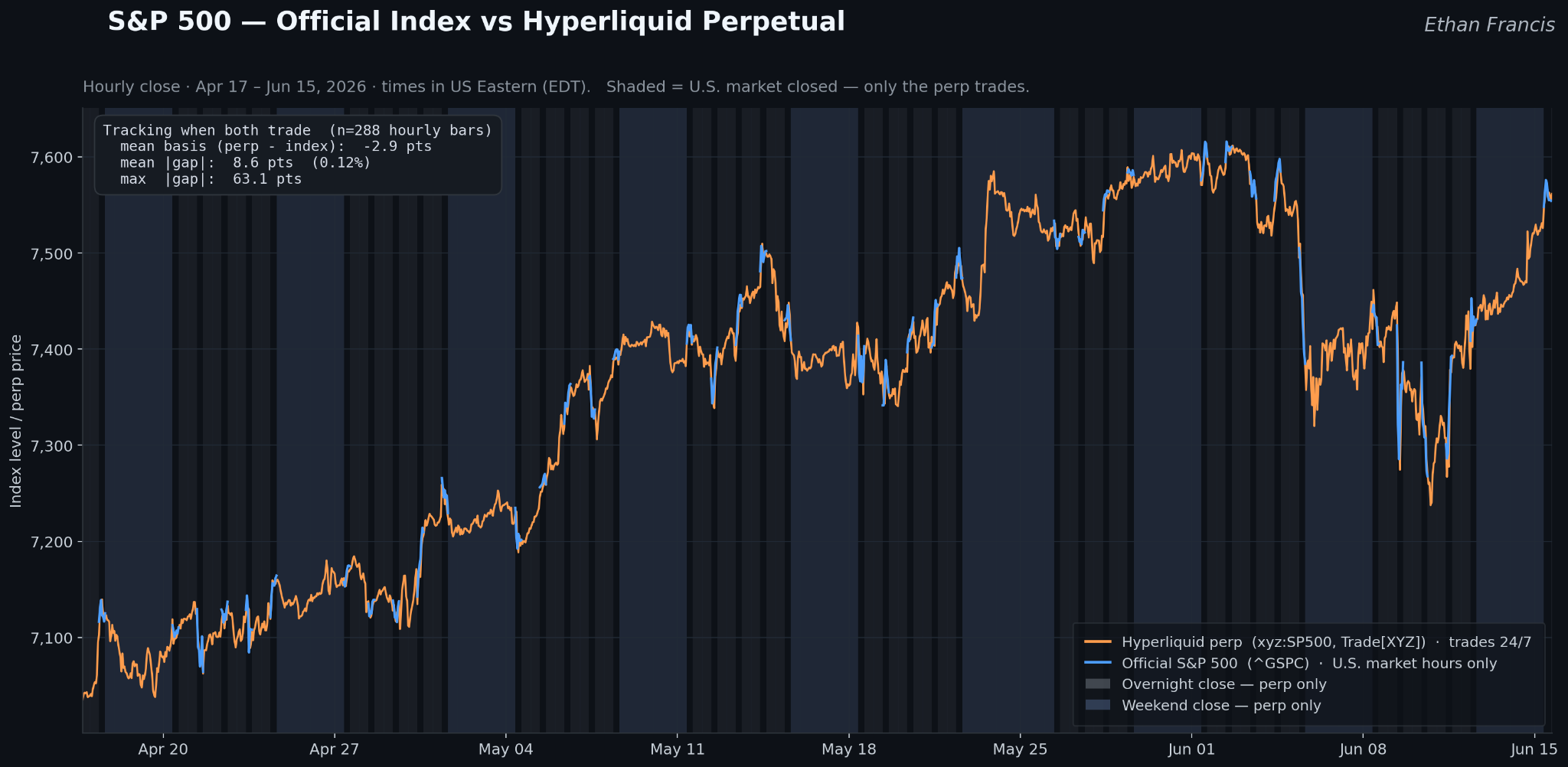

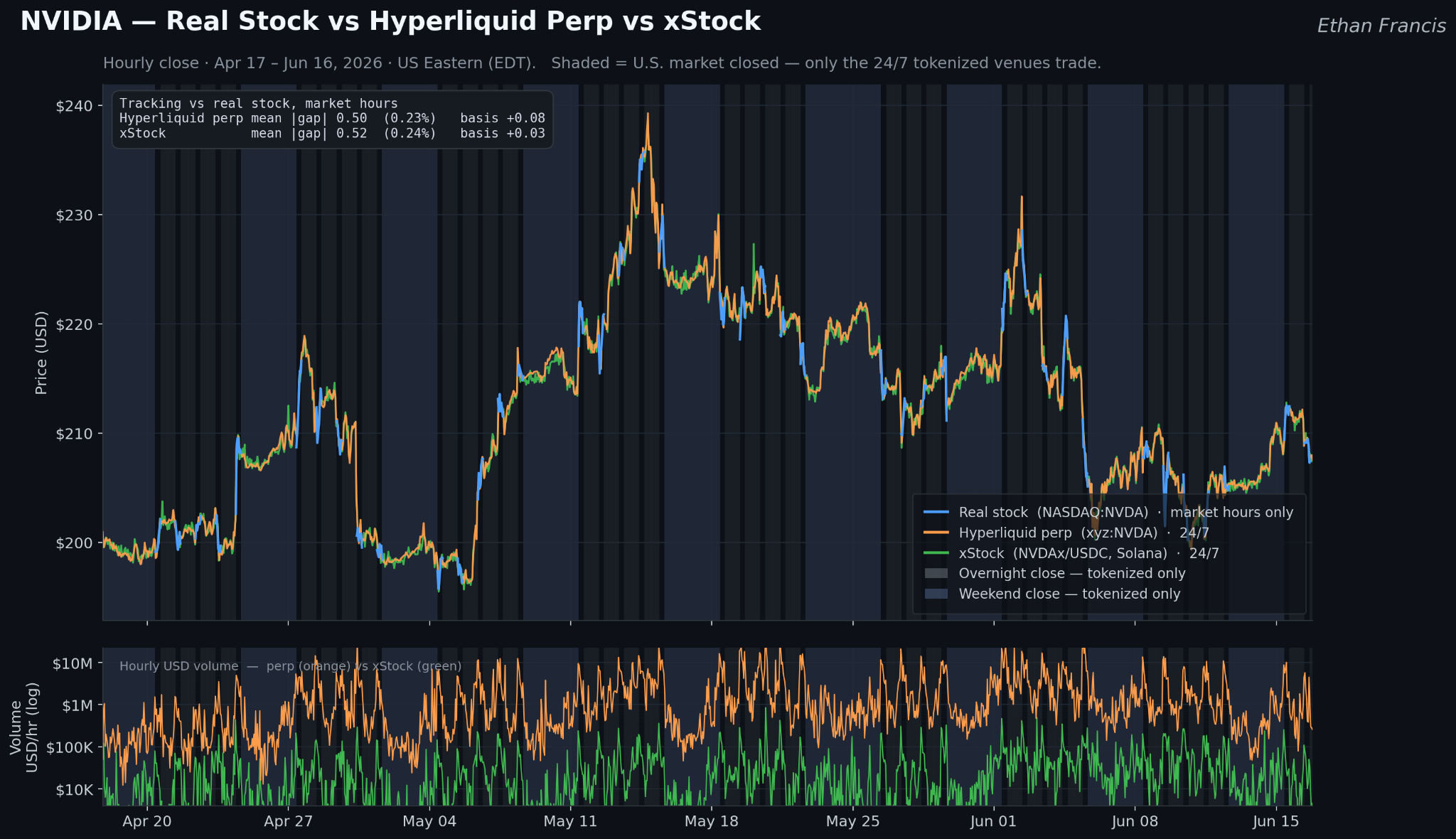

The missing key in this problem is onchain perps. Specifically, many equities markets have been deployed on Hyperliquid with HIP-3: roughly 50 that have sufficient volume and OI to be considered reliable for our use case.

Hyperliquid addresses these two critical problems I mentioned: providing us with a source of pricing, which is backed by considerable volume, through which we can actually hedge positions opened and closed during the weekend.

On Hyperliquid, the S&P generally has around $500M–$1B in daily volume, and as of writing this has roughly $350M in OI. This, unsurprisingly, leads to pretty accurate pricing! Now, this drops over the weekend, because pricing becomes untethered to an underlying cash market, but still has enough volume such that it can maintain a solid price-foundation, and, most importantly, allow us to hedge.

The strict price accuracy isn’t necessarily important to whether or not the stock can be traded, but it does determine the magnitude of demand. Obviously, if the price was unrealistic, no one would trade these assets over the weekend. But we can see that the perpetuals market is reasonably good at predicting the Monday open. If you take the relationship above and regress the realized opening gap, Monday’s open minus Friday’s close, against the perp’s move over that same weekend window, you get an R² of about 0.95.

Now, Street won’t just rip the price from any equity-linked market from Hyperliquid, we’ll run it through staleness checks and liquidity filters to only surface assets that we can realistically offer at-size. The vast-majority of stocks will not be tradeable on the weekend for this reason.

And to address the elephant in the room: many tokenized stocks do have DEX liquidity and thus will have prices that track through the weekend, but volume often lags significantly behind their Hyperliquid-counterparts, and thus is subject to more volatility, making it a mostly-unreliable means of pricing. They also have shallow liquidity, making it unsuitable for trading.

Buying NVDA on the Weekend

For Saturday and Sunday, we’ll be the market-maker for our selection of weekend stocks. By this, I’m referring to the fact that when a user buys or sells, we will protect ourselves from price deviation by opening a counter-position. If a user sells, we’re effectively long, so we open a corresponding short, and vice-versa. On market-open, both positions are closed and the upside in one fills the downside in the other, allowing us to be close-to-neutral.

The flow is relatively simple, let’s start by walking through a scenario where a user wants to buy 1 NVDA over the weekend:

- The NVDA price is quoted based on the reference market price: $210 for example.

- User submits a buy order at the price displayed, for 1 NVDA.

- We collect 210 USDC and “fill their order” at that quoted price, $210.

- The position is shown immediately to the user, albeit not minted onchain yet, but usable in a similar capacity (can be sold, but not transferred). The user has effectively prepaid at a set price, and they’ll capture corresponding price volatility from this point on.

- Now, because we’re “short” in that we owe the user 1 NVDA, we’ll adjust or open a corresponding long position.

- The market opens on Monday, and the price increases to $215. Our long-position covers the remainder, and we mint a token at $215, then it’s sent to the user.

- Or, alternatively, if the price decreases, we’ll be able to mint the token at a price lower than what the user paid, and thus still be delta-neutral.

| Action | Balance | Hedge |

|---|---|---|

| Before order | 0 USDC | 0 |

| User prepays $210 | 210 USDC | 0 |

| Street goes long NVDA on HL | 210 USDC | Long 1 NVDA ($210) |

| NVDA opens at $215 on Monday | 210 USDC | Long 1 NVDA ($215) |

| Street closes long position | 215 USDC | 0 |

| Street mints 1 NVDA and delivers onchain | 0 USDC | 0 |

In practice, we won’t be operating per-position, but rather have net positions open based on the buy and sell-side demand on Street that weekend. Rebalancing will happen in bands as-needed, and a large amount of small-orders can actually be filled by each other (orderbook matching).

And, this logic means that tokens bought over the weekend are effectively just price exposure instruments until the market opens, in which they’re delivered onchain and enter the user’s custody.

Selling NVDA on the Weekend

The logic for a sell-transaction is similar, with the caveat that we’ll hold a “float” to immediately pay users for their position, while opening corresponding shorts to hedge.

When a user sells NVDA, at $210, we’ll immediately give them 210 USDC in liquidity, and escrow that NVDA token onchain. This USDC comes out of a weekend float we maintain.

| Action | Float balance | Hedge | Escrow balance |

|---|---|---|---|

| Before order | $10,000 (low example float) | 0 | 0 |

| User sells 1 NVDA @ $210 | $9,790 | 0 | 1 NVDA token |

| Street goes short 1 NVDA on HL | $9,790 | Short 1 NVDA ($210) | 1 NVDA token |

| NVDA opens at $215 on Monday | $9,790 | Short 1 NVDA, −$5 unrealized | 1 NVDA token, worth $215 |

| Street redeems/sells NVDA at $215 | $10,005 | Short 1 NVDA, −$5 unrealized | 0 |

| Street closes short position | $10,000 | 0 | 0 |

One problem in supplying the sell-side liquidity for the weekend is a bank run. This can never be entirely avoided, unless you have infinite cash, but the loss of liquidity can be slowed, or largely prevented.

An easy way to do this is by using a degradation ladder, changing the logic of sell-side liquidity based on the remaining float.

For example, if our float remains >30% of our threshold, all transactions remain instant and provide immediate liquidity: with some high caps on total value set, such as $30K.

As this threshold drops, we apply a stricter cap to instant-liquidity transactions, and defer the rest: “deferred sell transactions” are transactions in which the sell-price is locked at the moment in which they sell it, but liquidity is delivered on Monday, which allows us to maintain a float balance for smaller orders.

Deferred transactions will be most common with very high-volume, asymmetric weekends. In market conditions outside of these, only very large sell transactions may be deferred, because between the float and adjacent buy-demand, the majority of sell transactions can be filled immediately.

But this degradation ladder can be applied in such a way that most users will have immediate liquidity if they desire to sell over the weekend, even in high-volume asymmetric conditions. And the users that don’t will still be able to sell at the price they choose.

By doing this we can preserve the economic outcome of all sell-side demand, while still providing a user experience equivalent to weekday-transactions for most.

This approach will allow trading on the weekend that, from a user experience standpoint, feels nearly-identical to trading on the weekday.

And, for us, if executed well, we’ll remain nearly delta-neutral and be able to fill the vast majority of orders instantly during Saturday and Sunday. This is a feature that requires mobile capital, which is okay, but it’s also a feature that isn’t necessarily a large revenue generator on its own, so I view it as CAC.

Not all users will find 24/7 particularly useful, especially because potential weekend price deviation is sub-par for short-term trading. But, there are some obvious reasons why many will find value in a weekend market.

One being opportunity cost. Strong news on the weekend will create buy demand, and bad news will create sell demand: a certain percentage of users will be willing to pay a potential premium for immediacy (whether for a legitimate strategic reason or spur-of-the-moment emotions).

And, mass-market retail often prioritizes timeliness, instead of waiting for perfect price execution.

Although it’s hardly a contrarian belief that 24/7 trading is valuable and is the next evolution of the equities market.

From 6.5/5, to 24/5, to 24/7.